Wealth is a Love Language: How Wills & Trusts protect your family during economic shifts.

- Alicia Anderson

- Mar 3

- 5 min read

Let's talk about something most people avoid until it's too late: what happens to the people you love when you're no longer here to provide for them?

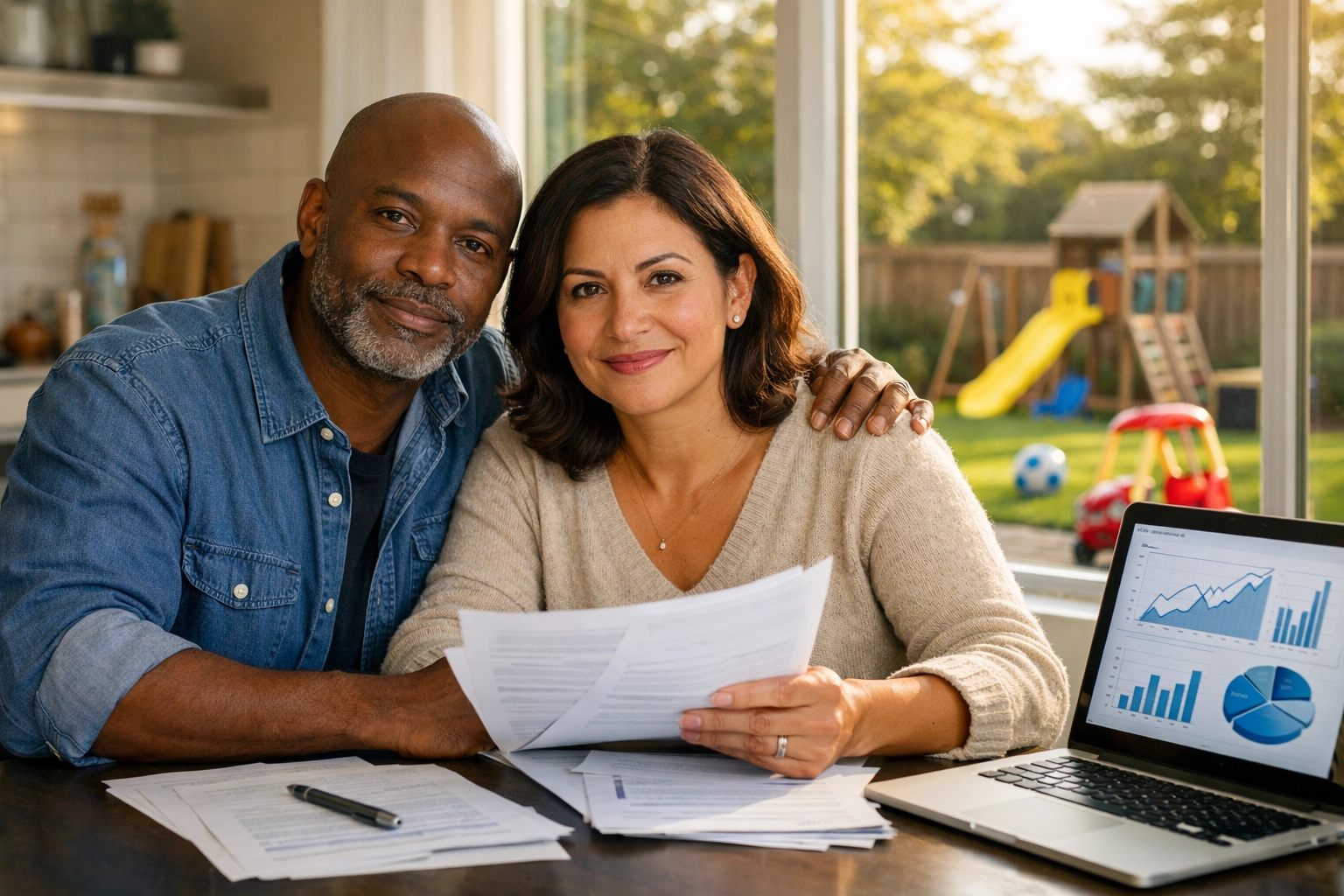

February is Love & Money Month, and if you truly love your family, one of the most powerful ways to show it isn't through grand gestures or expensive gifts. It's through strategic financial protection that outlives you. In times of economic uncertainty, when markets swing, inflation rises, and financial security feels fragile, your family needs more than hope. They need a plan.

That's where Wills and Trusts come in. These aren't just legal documents for the wealthy. They're love letters written in financial language, designed to protect the people who matter most when life throws curveballs.

Why Does Economic Uncertainty Make Estate Planning Urgent?

Here's a question: If the economy shifted tomorrow, if your business faced unexpected liability, if creditors came knocking, if your family suddenly needed access to resources but everything was tied up in probate, would your loved ones be protected?

Most families don't realize how vulnerable they are until crisis hits. Economic downturns don't just affect stock portfolios and retirement accounts. They expose gaps in estate planning that can cost families thousands in legal fees, months of waiting, and unnecessary stress during already difficult times.

When you establish a Will and Trust, you're not just dividing assets. You're creating a financial safety net that activates precisely when your family needs it most. During recessions, market crashes, or personal financial challenges, this protection becomes the difference between stability and chaos.

Trusts: Your Family's Financial Shield

Let me ask you something: Do you know what happens to your assets if you face a lawsuit, creditor claims, or business liability?

Without a trust structure, your personal wealth is exposed. Everything you've worked for, your home, savings, investments, can become vulnerable to legal claims and financial threats. This risk intensifies during economic downturns when businesses struggle and litigation increases.

Trusts create a legal barrier between your personal assets and external threats. When you place assets in a trust, they're no longer technically "yours" in the eyes of creditors. They belong to the trust entity, managed for your beneficiaries' benefit. This means if someone sues you, if your business faces challenges, or if you navigate divorce proceedings, your family's inheritance remains protected.

For business owners and professionals with liability exposure, this protection isn't optional, it's essential. Your wealth should support your family's future, not become collateral damage in legal battles or economic storms.

Avoiding Probate: Why Time Matters During Crisis

Here's what most people don't understand about Wills: they require probate. That means after you pass, your estate goes through a court process that can take months or even years before your family sees a dollar. During this time, assets are frozen, legal fees accumulate, and your family's financial needs don't pause.

Now imagine this scenario during an economic recession. Your family needs immediate access to resources for mortgage payments, living expenses, or emergency costs. But everything is locked in probate court while lawyers and judges process paperwork. How does that serve the people you love?

Trusts bypass probate entirely. Assets transfer directly to beneficiaries according to your instructions, without court involvement. No delays, no public records, no unnecessary legal expenses eating into their inheritance. During economic uncertainty when every dollar and every day matters, this efficiency protects your family's immediate financial security.

Controlled Distribution: Love Through Structure

Let me ask you this: Would you hand a teenager the keys to a luxury car with no driving lessons? Then why would you leave a lump-sum inheritance to beneficiaries without guidance on how to manage it?

One of the most overlooked benefits of trusts is controlled distribution. You decide exactly how and when your beneficiaries receive assets. Maybe your daughter is brilliant but financially inexperienced. Maybe your son struggles with impulse spending. Maybe your grandchildren are minors who shouldn't inherit significant wealth without oversight.

Trusts allow you to structure inheritance in ways that protect beneficiaries from themselves and from economic volatility. You can stipulate:

Distributions at specific ages or life milestones (graduation, marriage, starting a business)

Monthly or annual allowances rather than lump sums

Requirements for financial education before accessing larger amounts

Professional trustee oversight to guide investment decisions

This isn't about control from beyond the grave. It's about ensuring your wealth serves its purpose: providing long-term stability rather than short-term relief that disappears through poor decisions or economic downturns.

During recessions, families with structured trust distributions maintain financial security while others watch lump-sum inheritances evaporate through panic selling, debt payoff without strategy, or simply bad timing in volatile markets.

Tax Planning: Keeping Wealth in the Family

Every dollar that goes to taxes is a dollar that doesn't support your family. During economic shifts when every resource matters, strategic tax planning through trusts isn't just smart: it's an act of love.

Estate taxes can consume significant portions of larger inheritances, but trusts offer legal strategies to minimize this burden. For families with substantial assets, tools like generation-skipping trusts allow wealth to pass directly to grandchildren, removing asset growth from taxable estates and preserving capital across multiple generations.

Even if your estate isn't currently large enough to trigger federal estate taxes, state-level taxes and future legislative changes could affect your family. Establishing trust structures now provides flexibility to adapt as tax laws and economic conditions evolve.

The question isn't whether you can afford estate planning. It's whether your family can afford for you not to have it.

Ongoing Management: Protection During Incapacity

Here's something most people don't consider: estate planning isn't just about death. What happens if you become incapacitated: unable to make financial decisions due to illness, injury, or cognitive decline?

Without a trust, your family faces court proceedings to establish guardianship or conservatorship just to access and manage your assets. During economic volatility when investment decisions matter daily, this delay can be financially devastating.

Trusts activate immediately upon incapacity, allowing your designated trustee to step in and manage assets without court involvement. Your bills get paid, investments get managed, and your family maintains financial stability while you focus on health and recovery.

This continuity of management protects your wealth from neglect during vulnerable periods and ensures professional oversight when your family needs it most.

Questions to Consider for Your Family

Let me leave you with some questions that deserve honest answers:

If something happened to you tomorrow, would your family know how to access the resources they need?

Are your assets protected from creditors, lawsuits, and economic threats?

Do you have minor children who would need guardianship and financial management?

Are there beneficiaries in your family who might struggle with managing a large inheritance?

Have you structured your estate to minimize tax burden and maximize what reaches your loved ones?

Does your plan account for incapacity, not just death?

If any of these questions make you uncomfortable, that discomfort is information. It's your intuition telling you that the people you love deserve better protection.

Building Your Legacy Today

At Personal Development Groups, we believe wealth isn't just about accumulation: it's about strategic protection and purposeful transfer. Wills and Trusts aren't morbid topics to avoid. They're powerful tools that allow you to care for your family long after you're gone.

Economic shifts are inevitable. Market volatility, recessions, and financial challenges will come. But your family's security doesn't have to be left to chance. When you establish comprehensive estate planning, you're not just protecting assets. You're protecting peace of mind, family stability, and the legacy you've worked your entire life to build.

The best time to plan was yesterday. The second best time is now. Because love isn't just what you feel: it's what you do to protect the people who matter most, even when you can no longer be there to do it yourself.

Follow for daily money tips + business building

Comments